Tech is no longer the moat. Here is what replaced it.

Everyone has AI. So what now?

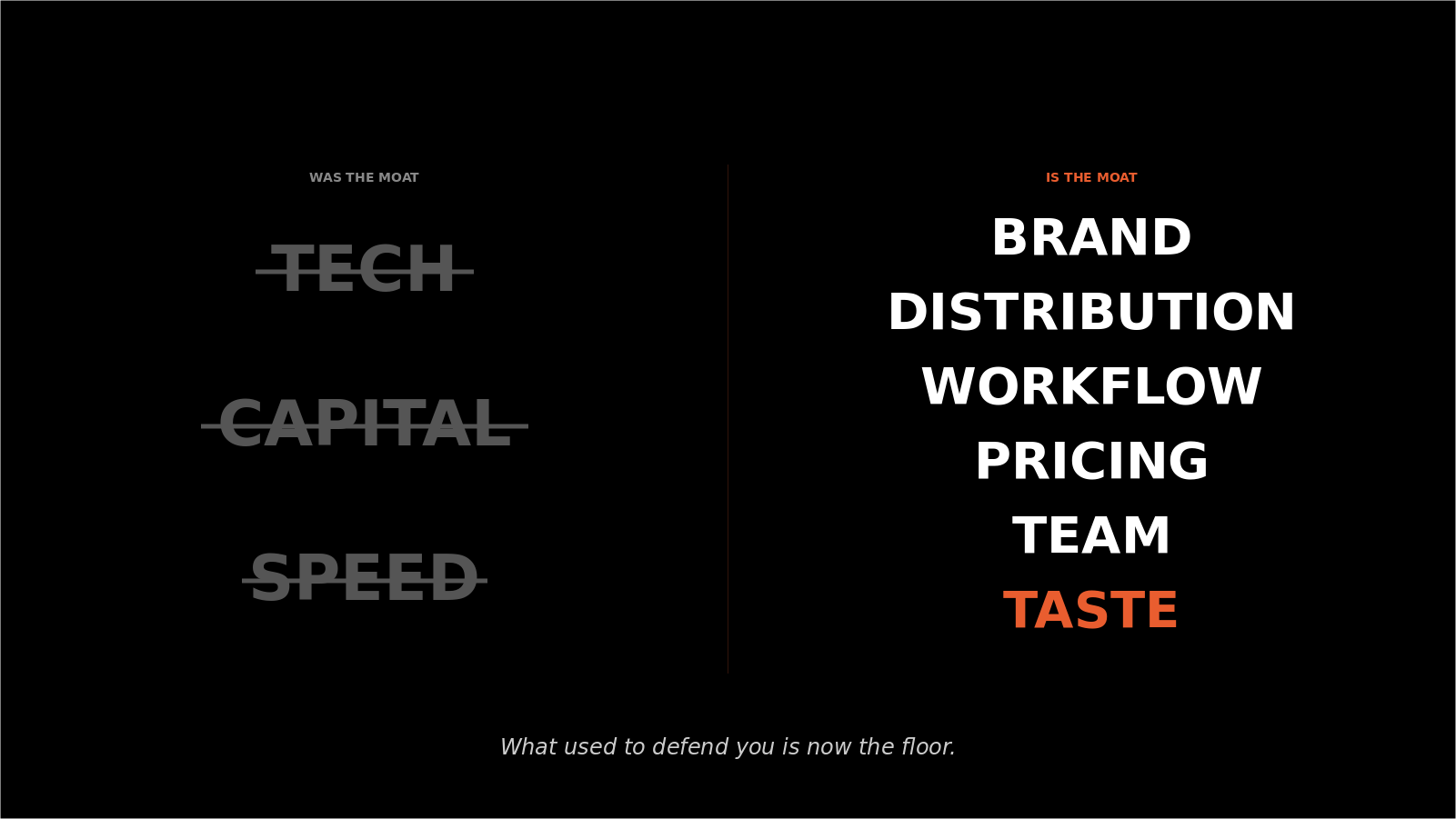

Every market now has ten lookalikes shipping the same features in the same quarter. Same models underneath. Same wrappers on top. Same launch posts on Product Hunt and LinkedIn the next morning. If that’s the world you’re competing in, your moat is the problem. Not marketing. Not sales. Not the product itself. The old moats are gone. Technology stopped being defensive once everyone could call the same APIs. Speed-to-build stopped being defensive once a single engineer could ship in a weekend what used to take a quarter. Even capital stopped being defensive once the cost to launch dropped to almost nothing. Your edge gets cloned in months, not years. The whole game has shifted.

Three forces compressed the old playbook in 2026.

The first: AI lowered the cost to ship. No-code builders, agentic workflows, vibe coding, design templates. The bar to put a working product in front of users collapsed from years to weeks. The product is no longer the hard part. It’s the floor.

The second: PMF half-life collapsed. Product-market fit used to be a destination. Find it, then scale. Now it’s a moving target. ChatGPT’s consumer share dropped from 78.6% to 74.3% in a single year (a16z, January 2026). Even category leaders lose share quarterly. Your edge melts every time a new model drops, and a new model drops every quarter.

The third: distribution channels splintered. Search is fragmenting. AEO (Answer Engine Optimisation, the practice of showing up in AI-generated answers) is replacing SEO. Your buyer doesn’t open Google anymore. They ask ChatGPT, Perplexity, or Gemini. The funnel of 2018 is dead, and most companies are still budgeting against it. When the floor rises this fast, the moat has to move up the stack.

The companies that compound through 2026 are not the ones with better technology. They are the ones who saw the moat shift and rebuilt around it

The six moats that replaced technology

That sentence is from the GTMfund Moat Series, and it has been spreading among operators across Europe and the US. It captures something most companies feel but haven’t named. Here is what we’d add: there is more than just brand and distribution. Six things have replaced “we have AI” as the things that actually defend a company. Here they are.

None of these are about technology. All of them are about how you operate, what you stand for, and how you ship.

Brand & POV.

If you can’t put your point of view on a billboard, you don’t have a brand. You have a logo.

Linear charges 2× what Jira does and wins, not because the feature list is longer, but because the product has a clear opinion about how engineering teams should work. In a world where everyone uses the same models, the brand with the clearest point of view wins. Have one, or get cloned.

Distribution & Discovery.

Your buyer doesn’t Google anymore. They ask ChatGPT, Perplexity, or Gemini.

AEO (Answer Engine Optimisation) is the new SEO, and most companies haven’t started thinking about it. The window is open right now. It will close. Pipeline that depends on someone else’s algorithm is a moat made of sand.

If you are not in the answers, you are not in the conversation.

Workflow Depth.

Wrappers die. Embedded workflows compound.

GPT call in, formatted output back, sold as a product runs fine in the demo and dies in the renewal conversation. Notion, by contrast, knows your team’s templates, your meeting structures, your specs. The longer you use it, the harder it is to leave.

Your moat is the data your customer cannot get anywhere else.

Pricing & Margin.

Stop pricing AI like it’s 2018 SaaS.

Per-seat pricing made sense when the seat did the work. Decagon charges per ticket resolved. Cursor blends seats with usage. Bessemer data shows the fastest-growing AI applications, the Supernovas, average around 25% gross margin. Without pricing discipline, expansion revenue burns covering compute.

Align price with value, or watch your margins evaporate.

Team Shape.

The five-person company is the new playbook.

Bessemer’s AI Supernovas average $1.13 million in ARR per employee. AI-native GTM teams are 38% leaner than traditional SaaS and reach $10 million ARR three times faster (Growth Unhinged). One senior operator with the right AI stack does what used to take a team of five.

If you are hiring like it’s 2021, you are already behind.

The shift is especially visible in marketing. In 2021, growth, content, SEO, brand, PR, community, partnerships, product marketing, and creative often meant separate roles or teams. In 2026, many of those functions collapse into a smaller GTM pod, led by a senior operator and amplified by AI agents across research, copy, analytics, outreach, and workflow operations. The team is not just smaller. It is more integrated, faster, and closer to revenue.

Speed & Taste.

Anyone can ship. Few ship something people love.

Vibe coding made prototyping 20× faster. Speed has commoditised. The bottleneck has moved. It is now taste: knowing what to build, what to leave out, what feels right. Linear says it cleanly: speed is a feature. That obsession is why teams pay 2× the price.

Speed gets you to market. Taste keeps you there. Most companies pick one.

Everyone has AI. The winners have a point of view.

You can’t out-build your way out of commoditisation. You can out-think it.