Hyper growth is the new vanity metric.

The record keeps breaking. The prize keeps shrinking.

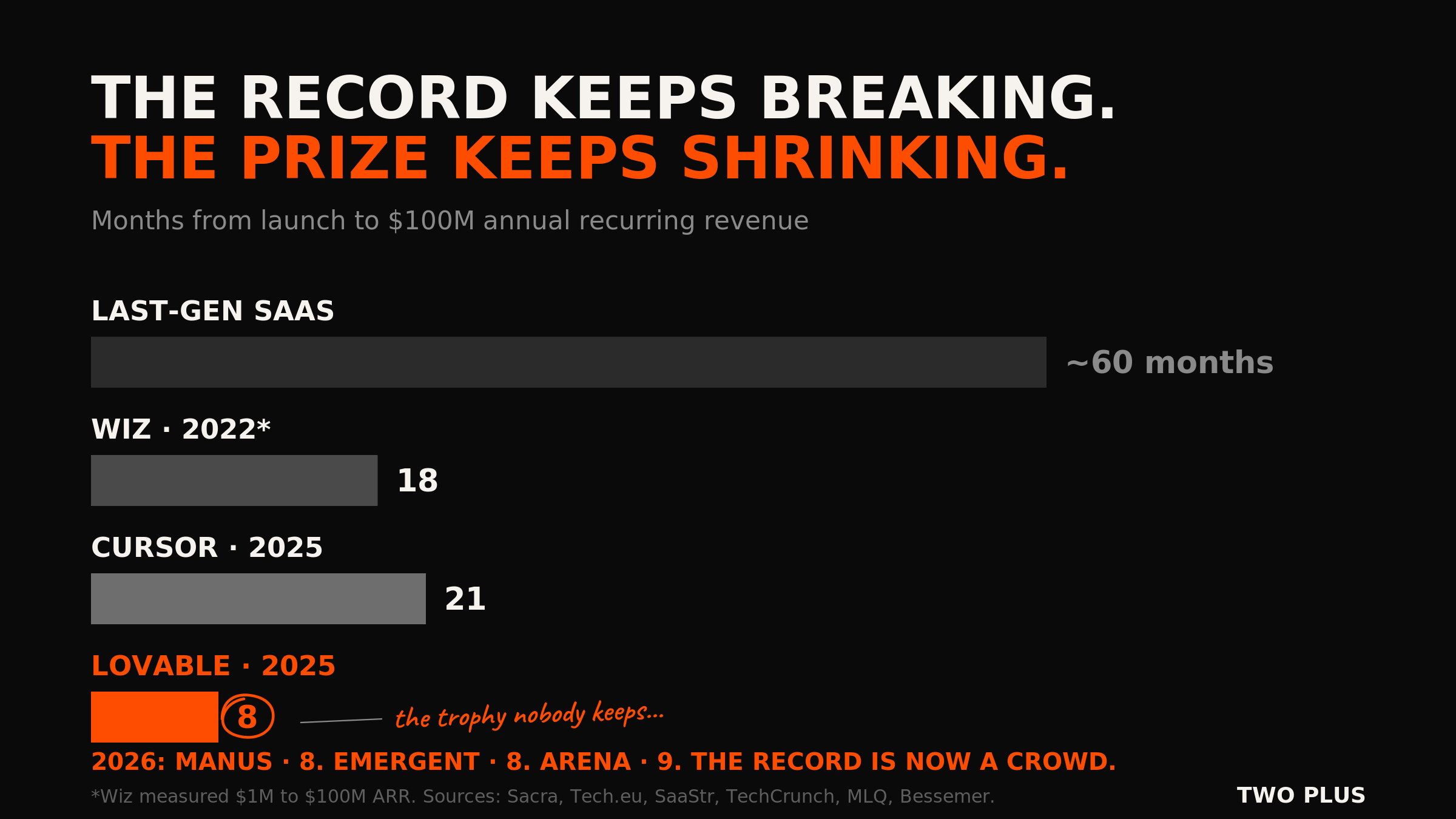

In the last SaaS generation, reaching $100 million in annual recurring revenue (ARR) inside five years made you a case study. Wiz compressed it to eighteen months and broke the record. Cursor did it in about twenty-one months from launch and broke it again. Lovable did it in eight. Within a year, Manus and Emergent both claimed the same eight-month mark, Arena claimed nine, and the record stopped being a record. It became a tie nobody can verify.

If you're watching those numbers and concluding you're behind, look closer. The same cohort that is shattering every growth record in software history is also posting the worst retention numbers the industry has ever measured. Both things are true at once, and the second one decides who's still here in 2028.

Speed is not the signal anymore. If your company is growing fast and you still feel exposed, you are not having a growth problem. You are having a staying problem.

The fastest cohort in history

The leaderboard is real, and it's worth taking seriously before we take it apart.

Cursor passed $100 million ARR in January 2025 (Sacra), then kept compounding: past $500 million by mid-2025 and past $1 billion by late 2025 (SaaStr). Lovable went from public launch to $100 million ARR in eight months (Tech.eu, July 2025) and reached roughly $400 million ARR by February 2026 with 146 employees. Bolt put up $40 million ARR within six months of launch. Bessemer's State of AI report tracks a whole class of these companies, the Supernovas, averaging $40 million in first-year ARR.

And it hasn't slowed. Manus matched Lovable's eight months before selling to Meta for over $2 billion. Emergent, a vibe-coding platform out of India, claimed the same eight-month mark in February 2026 (TechCrunch). Arena did it in nine. Even enterprise software joined in: Legora became the fastest enterprise business to $100 million, eighteen months, per Bessemer in April 2026.

Cursor's record, by the way, stood for about six months. Nobody frames the trophy anymore. There are now at least three companies with a legitimate claim to "fastest ever," which tells you everything about what the title is worth.

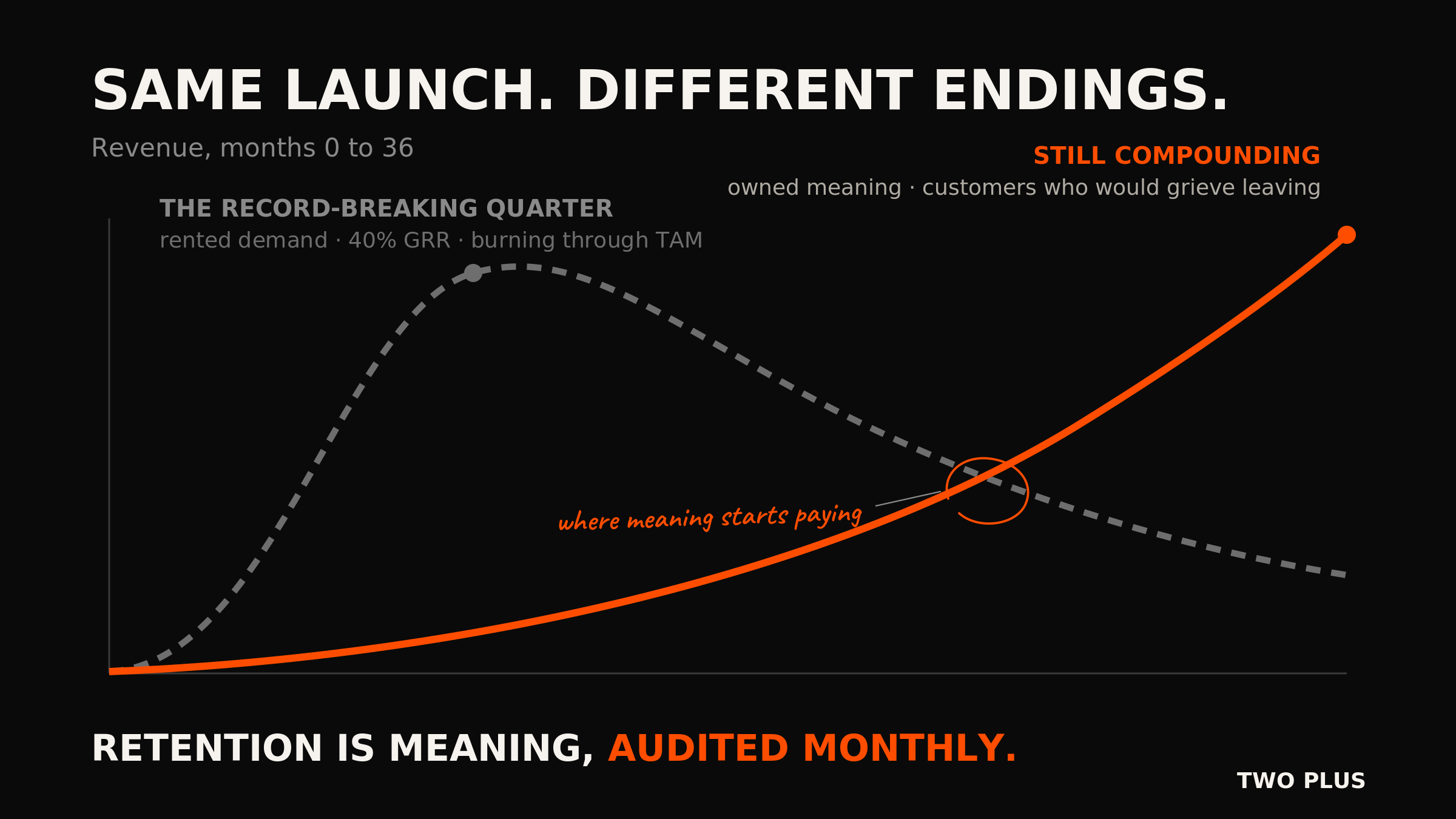

Set that against the previous generation, where $100 million took most winners the better part of a decade, and the conclusion looks obvious: a new species of company has arrived. Except the trajectory chart only has one line on it. Add the second line, the one that shows who keeps the revenue, and the picture changes completely.

The other line on the chart

Jasper is the cleanest version of the story. An AI writing tool that hit roughly $120 million ARR at peak and a $1.5 billion valuation in October 2022, one of the fastest-growing software companies of its moment. ChatGPT launched a month later. Customers replaced their $50-a-month Jasper subscriptions with a free chatbot, the 2023 revenue forecast was cut by around 30%, and the company wrote down its own valuation. Jasper survived by rebuilding as an enterprise product, but the original rocket ship is gone.

That was supposed to be a cautionary tale about thin wrappers. It reads more like a preview.

Bolt's CEO Eric Simons said it plainly in an interview about the vibe-coding market: "Everyone has one problem right now, a very high level of customer churn. We need to build a business that retains, not just collects quick subscriptions." That's a CEO at the front of the fastest product category in software describing the entire category. Reports through early 2026 show Replit, Lovable and Vercel's v0 all shedding users behind the headline curves: the flood of people who discovered they could build something, followed by the retreat of people who discovered they couldn't maintain it. A user base like that isn't an install base. It's a departure lounge.

The pattern is general. The engine that produces record-breaking growth, near-zero friction to try, near-zero friction to pay, is the same engine that produces record-breaking churn. Easy to buy is easy to cancel.

The tourist problem

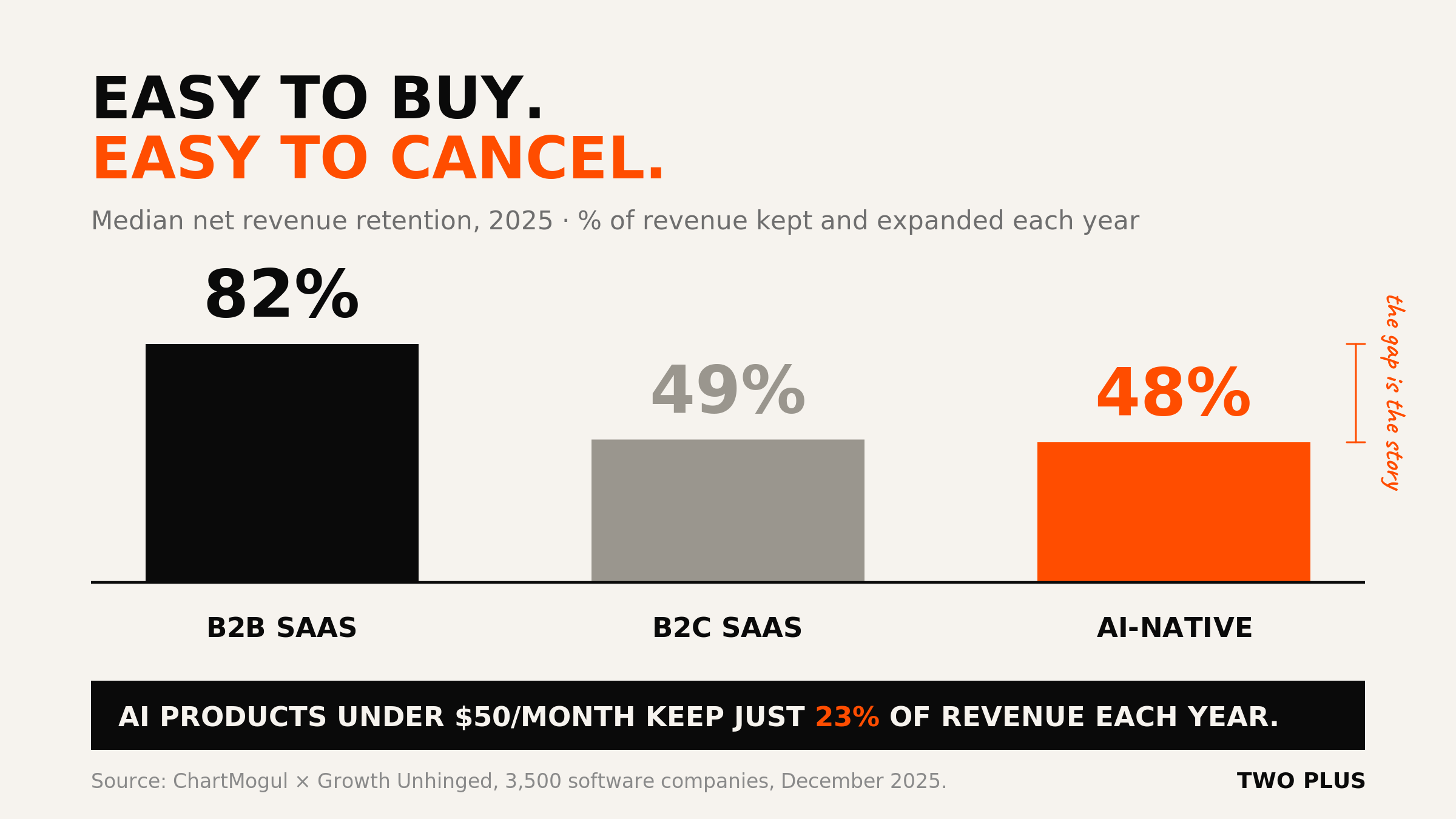

In December 2025, Kyle Poyar and ChartMogul published retention data across 3,500 software companies, and it put numbers on what operators were already feeling.

B2B SaaS holds a median net revenue retention (NRR, the revenue you keep plus expansion) of 82%. AI-native companies show a median NRR of 48%, with gross revenue retention (GRR, what you keep before any upsell) at just 40%. Worse than consumer subscriptions. For AI products priced under $50 a month, median GRR falls to 23% (ChartMogul × Growth Unhinged, December 2025).

Read that slowly. The median AI-native company loses more than half its revenue base every year and replaces it with new customers. That's not recurring revenue. That's demand you rent. The growth chart looks identical to the compounding kind right up until acquisition slows, and then, in Poyar's phrase, you discover you've been burning through your TAM (total addressable market: the pool of buyers you get to lose exactly once). Cassie Young at Primary Venture Partners calls what comes next a "gross retention apocalypse."

The same dataset carries the counter-signal. Companies with low NRR are three times more likely to be shrinking than growing quickly, while the AI-native companies that reach durable scale show roughly double the GRR of their early-stage peers. The winners aren't the ones who grew fastest. They're the ones who kept what they grew.

Same speed. Different endings.

So what separates the fast companies that hold from the fast companies that melt? Not model access. Everyone calls the same APIs, as we argued in the moats piece. Not features, which get cloned in a quarter. Not funding, which Jasper had plenty of.

Look at the companies whose curves keep compounding and a different variable shows up. Character. A specific, consistent answer to the question of what the product believes, and meaning that accumulates in the customer's work rather than novelty that wears off.

Linear charges twice what Jira does and keeps winning renewals, because the product carries an opinion about how engineering teams should work and every pixel agrees with it. Notion holds its customers because a team's templates, wikis and ways of working pile up inside the product until leaving means abandoning part of how the company thinks. Duolingo turned a commodity, language drills, into a decade of daily habit by wrapping it in character, streaks and identity, and it keeps growing while feature-identical competitors cycle through users. Perplexity walked away from an in-product advertising business that would have printed money, because the service means "answers you can trust" and ads would quietly unsay it.

None of these companies won on trajectory. Several were slower than their rivals in year one. All of them built products that stand for something specific, and that their customers would have to give up a piece of their own workflow, habit or identity to leave.

Come for the novelty, stay for the quality and trust. That has always been the arc of a durable customer relationship. What changed is the economics of each half: the novelty half has never been cheaper to produce, and the staying half has never been rarer.

That's the mechanism the retention data is measuring. Retention is meaning, audited monthly. A customer renews when the product has become part of how they work or who they are, and churns when it was only ever a capability, because capabilities get commoditised and meaning doesn't.

Ask yourself

Five questions, in place of a growth review. Be honest.

If your product's capability shipped inside ChatGPT tomorrow, what would your customers stay for?

What accumulates inside your product with every month of use that a customer would grieve losing?

Can your team state, in one sentence, what the product believes that competitors don't?

What revenue would survive a quarter with zero new logos?

Have you ever said no to money because it contradicted what the service means? Perplexity has. Most companies never face the question because they never decided what the service means.

If your answers lean on speed, features or the model, you're renting your demand. The lease ends at the next model release.

The bottom line

Growth used to be expensive, so growth was the proof. It took years of distribution-building to reach $100 million, and the number certified everything underneath it. Now the number arrives in eight months, the infrastructure that produces it is available to everyone, and the median company renting that infrastructure loses 60% of its revenue base a year.

Speed tells you the market noticed. Retention tells you it cared.

The companies that own the next decade will grow fast, most things do now. What will distinguish them is that they decided early what their service means, built character into every surface of it, and let that meaning accumulate in their customers' work until leaving stopped making sense.

Fast is the entry fee. Staying is the business.